If you’re an Australian aiming for early retirement (or even just flexibility before 60), you’ve probably realised something frustrating pretty quickly:

Most “retirement planning tools” aren’t actually built for early retirement - or for the way Australians really build wealth.

Some tools are powerful but not fully Australia-aware. Others understand super and pensions only help you plan for retirement at 60 with super.

Below is a practical comparison of the most commonly used financial planning tools Australian's turn to when thinking about early retirement - what they do well, where they fall short, and who they’re really for.

The Tools We Compared

- Excel (DIY, Aussie FireBug Spreadsheet)

- ProjectionLab

- Government & Super Fund Calculators (ASIC MoneySmart Retirement Planner, SuperCalcs, AMP Retirement Simulator)

- Financial Mappers

- Canwi

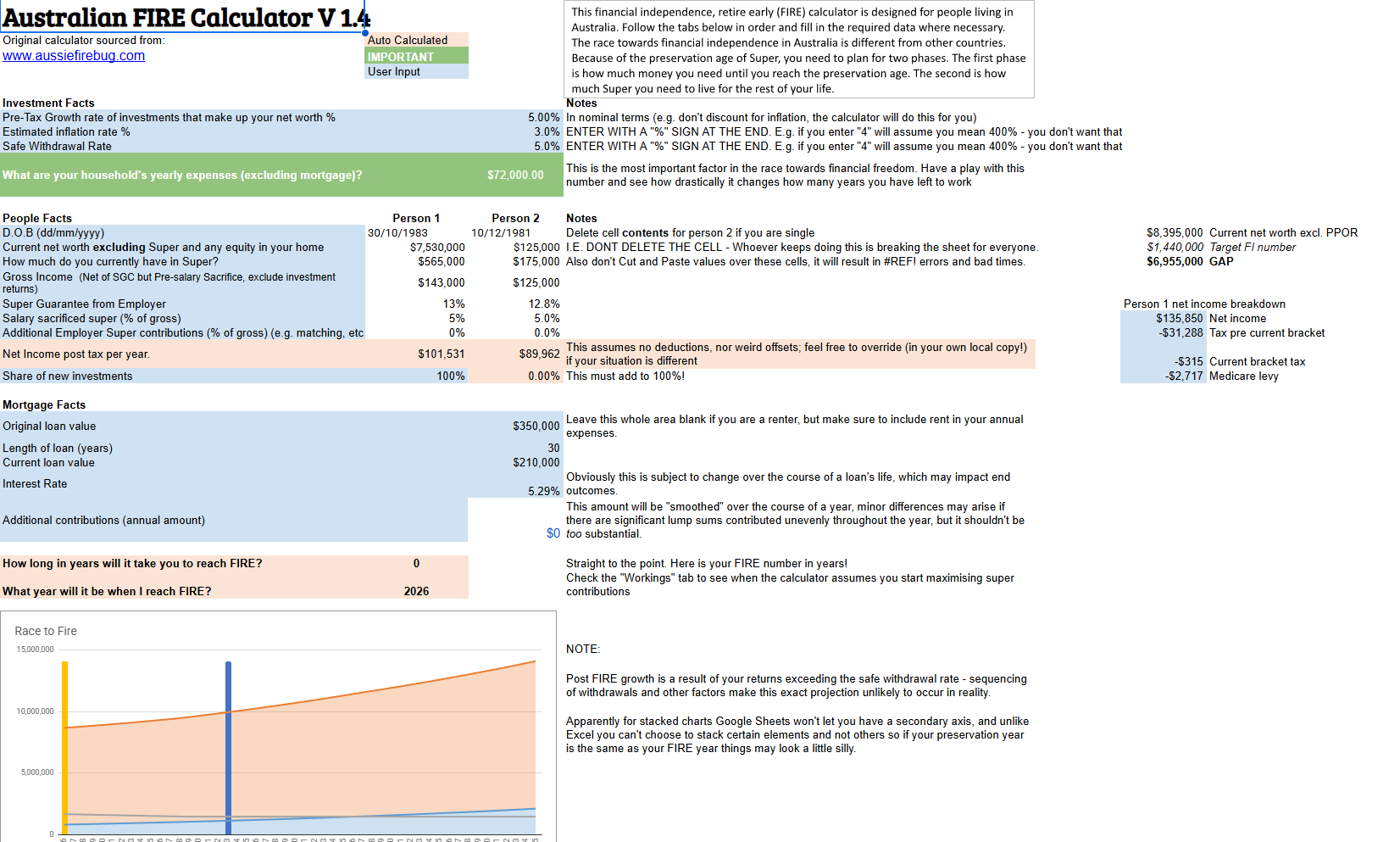

Excel

(DIY, Aussie FireBug Spreadsheet)

For many Australians - especially those pursuing FI/RE or trying to make a specific financial decision - Excel (or google sheets) is the first real "financial planning tool" you'll use.

We LOVE excel, its flexible, powerful and if you can imagine a model, depending on how good your excel skills are... you can build it.

That's both its biggest strength - and its biggest weakness

✅ Pros

- Total flexibility - you can model almost anything

- No baked-in assumptions - every formula is yourse

- Free / familiar - especially for analytical / corporate folks

- Lots of templates and shared models (e.g the Aussie Firebug spreadsheet)

⚠️ Cons

- Becomes fragile as it grows in complexity

- Most people will struggle to model interdependent decisiosn (tax, super, cashflow interacting)

- Hard to adapt or take into account all the rules (tax, super caps, etc)

- Only shows what you already know to model - doesn't tell what you've missed.

Best for:

Confident DIYers who enjoy building and maintaining their own models, but it’s less suited to people who want guided, robust planning that adapts as life and rules change.

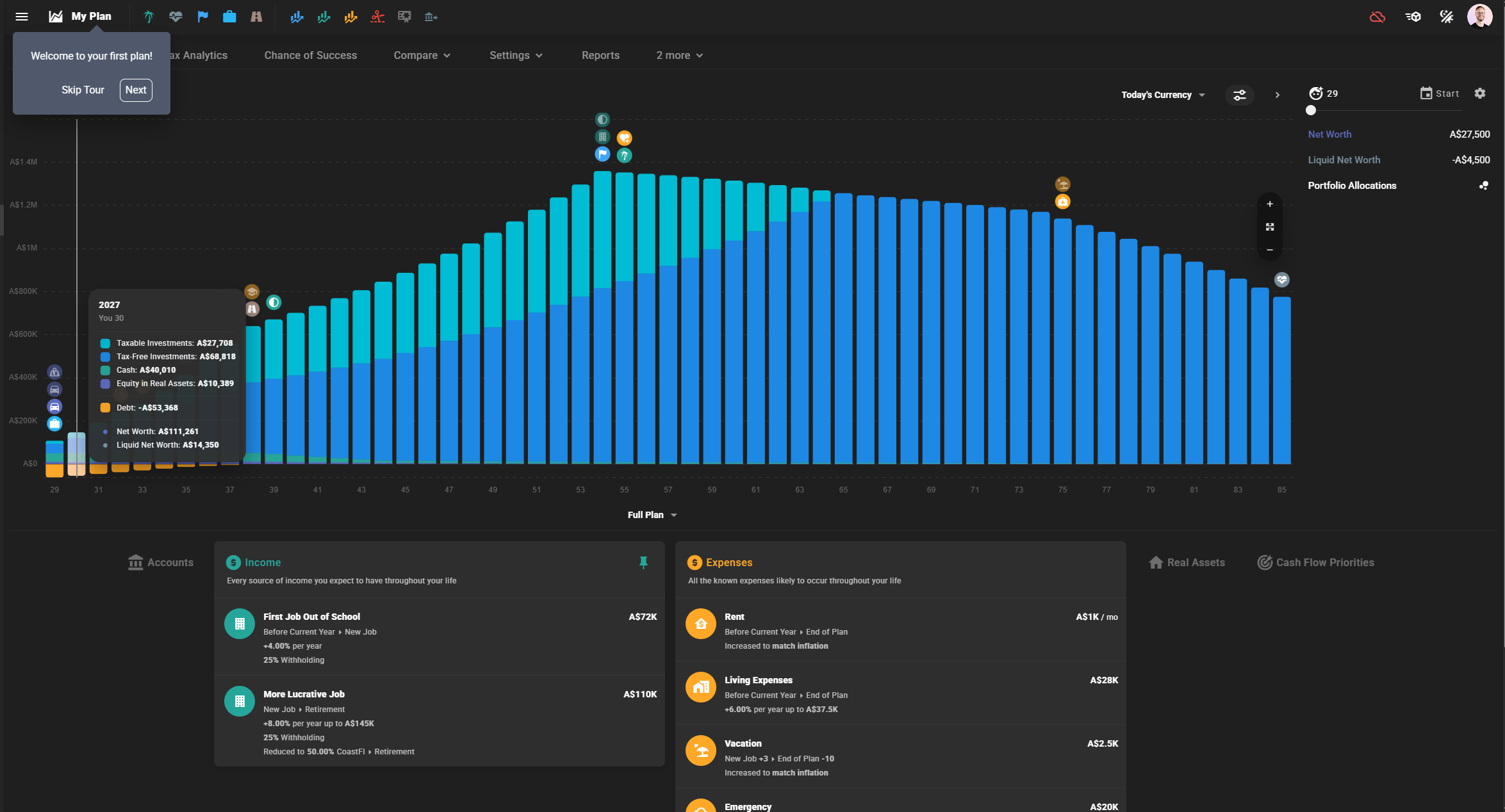

Projection Lab

ProjectionLab is one of the most capable consumer-accessible retirement modelling tools available. It shines when it comes to:

- Multi-scenario planning

- Long-term cashflow projections

- Monte Carlo simulations

- Historical backtesting

- Clear visualisation of trade-offs

For people pursuing FIRE, it’s one of the better tools globally.

✅ Pros

- One of the most powerful consumer retirement modelling engines globally

- Excellent long-term cashflow projections and visualisations

- Strong support for scenario comparison and “what-if” analysis

- Includes advanced features like Monte Carlo simulation and historical backtesting

- Flexible enough to model complex early-retirement paths

⚠️ Cons

- Generally assumes the user already knows the strategy and how to implement it

- Doesn't natively support Australia's financial system, there's limited supported with marginal tax rates, but “workarounds” for mimicing super drawdown rules (e.g. configuring a Roth IRA to mimic super drawdown rules)and support for downsizer contributions or 6 year rule exemptions on property CGT add friction and complicate the experience

- Built around financial entities rather than life events, meaning real-world plans like pay rises or buying a property need to be translated into Planned Assets and Debts.

- Major life decisiosn don't automatically account for their real-world costs - users need to identify, do the research and calculate costs for things like stamp duty and purchase expenses themselves

Best for:

People who want a powerful projection engine and are willing to manually implement Australian rules and strategies themselves.

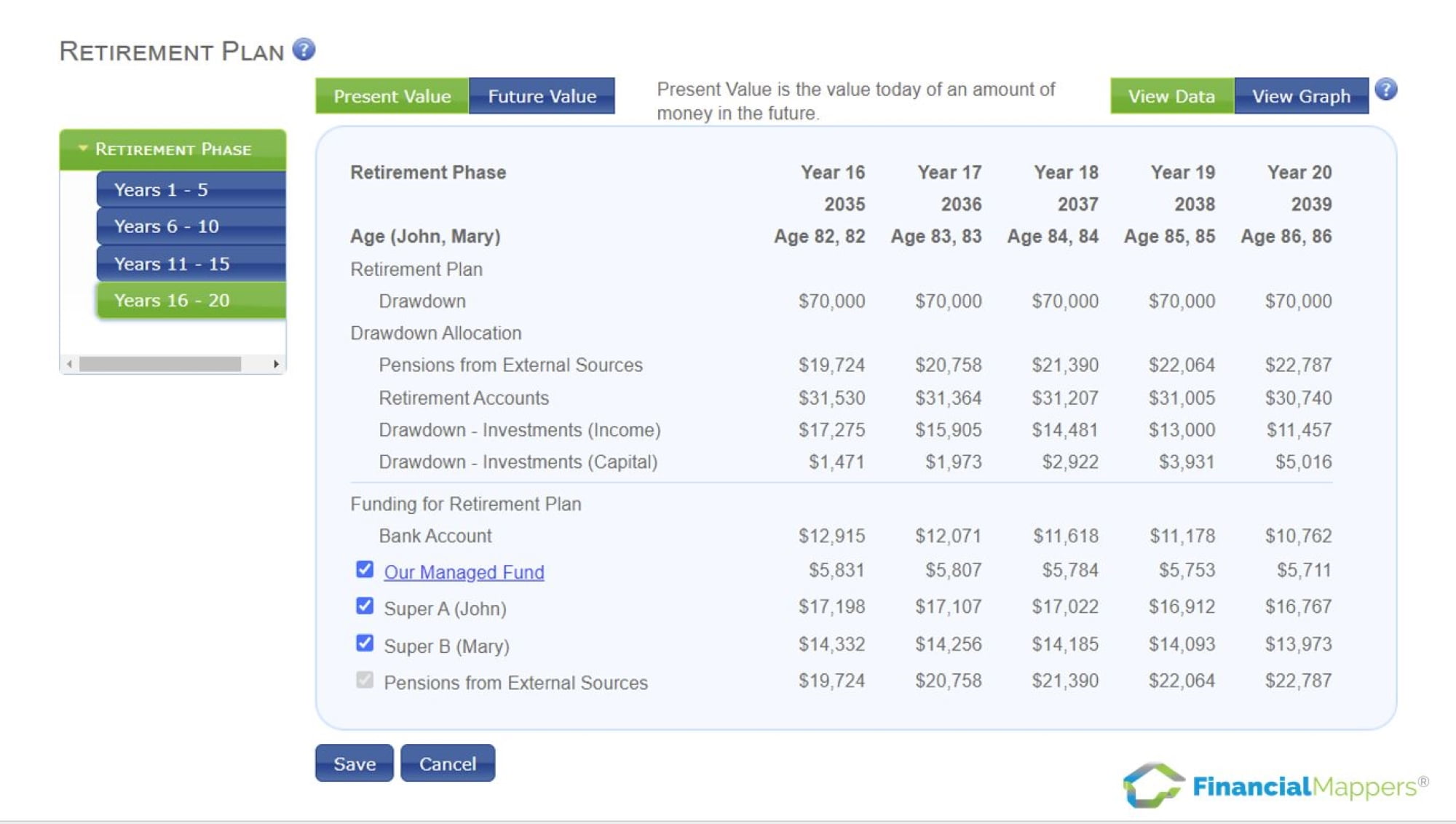

Financial Mappers

Financial Mappers is one of the few Australian tools on this list.

It offers:

- Detailed cashflow modelling

- Multi-year projections

- Strong adviser-grade logic

- Flexibility to model complex scenarios

✅ Pros

- Strong cashflow-based modelling with a clear focus on long-term projections

- Designed specifically for the Australian financial system

- Handles complex scenarios, multiple income streams, assets, and liabilities well

- Flexible enough to model non-linear life paths and changing assumptions

- Depth that appeals to advisers and highly engaged DIY planners

⚠️ Cons

- The platform assumes a high level of financial literacy from the user

- Planning is driven by detailed financial inputs rather than life events or decisions

- Users need to decide:

- what to model

- when to model it

- and how different components should interact

- Insights tend to emerge after significant setup, rather than being guided upfront

- Can feel closer to professional modelling software than a consumer planning tool

Best for

Highly engaged planners or advisers who want deep, Australia-specific cashflow modelling and are comfortable doing the thinking, structuring, and interpretation themselves.

Government & Super Calculators (ASIC MoneySmart, SuperCalcs & AMP etc)

Excellent for Quick Checks, Not Nuanced Planning

Tools like the ASIC MoneySmart Retirement Planner, SuperCalcs, and the AMP Retirement Simulator play an important role in the Australian financial ecosystem.

They’re widely trusted, easy to access, and intentionally simple — which is exactly why so many Australians start with them.

These tools are best thought of as confidence checks, not comprehensive financial planning platforms.

✅ Pros

- Provide clear, high-level retirement income estimates

- Model super balances and pension-style outcomes

- Help answer the question: “Am I broadly on track?”

- Require very little setup or financial knowledge

- Offer reassurance for people approaching traditional retirement ages

- For someone wanting a quick, sensible snapshot - particularly later in life - they do their job well.

⚠️ Cons

- Designed to be rigid and simplified by intent

- Assume fairly standard, linear life paths

- Optimise for clarity over flexibility

As a result, they typically:

- Assume retirement starts at or after preservation age

- Rely on linear income and spending assumptions

- Offer limited ability to:

- retire before 60

- vary work patterns (part-time, sabbaticals, coast FIRE)

- model nuanced drawdown strategies across multiple asset types

- Calculation methods can also be hard to discern or require reading lengthy disclaimer docs. For example, some tools (including SuperCalcs) estimate income from non-super assets using Age Pension deeming rules, rather than modelling asset sales, dividends, or realistic investment income - an approach that can materially understate flexibility, especially for early retirees relying on investments before super access.

Best for

People who want a fast, trustworthy sense check of their retirement position - particularly those nearing traditional retirement age - rather than a tool for exploring complex or early-retirement strategies.

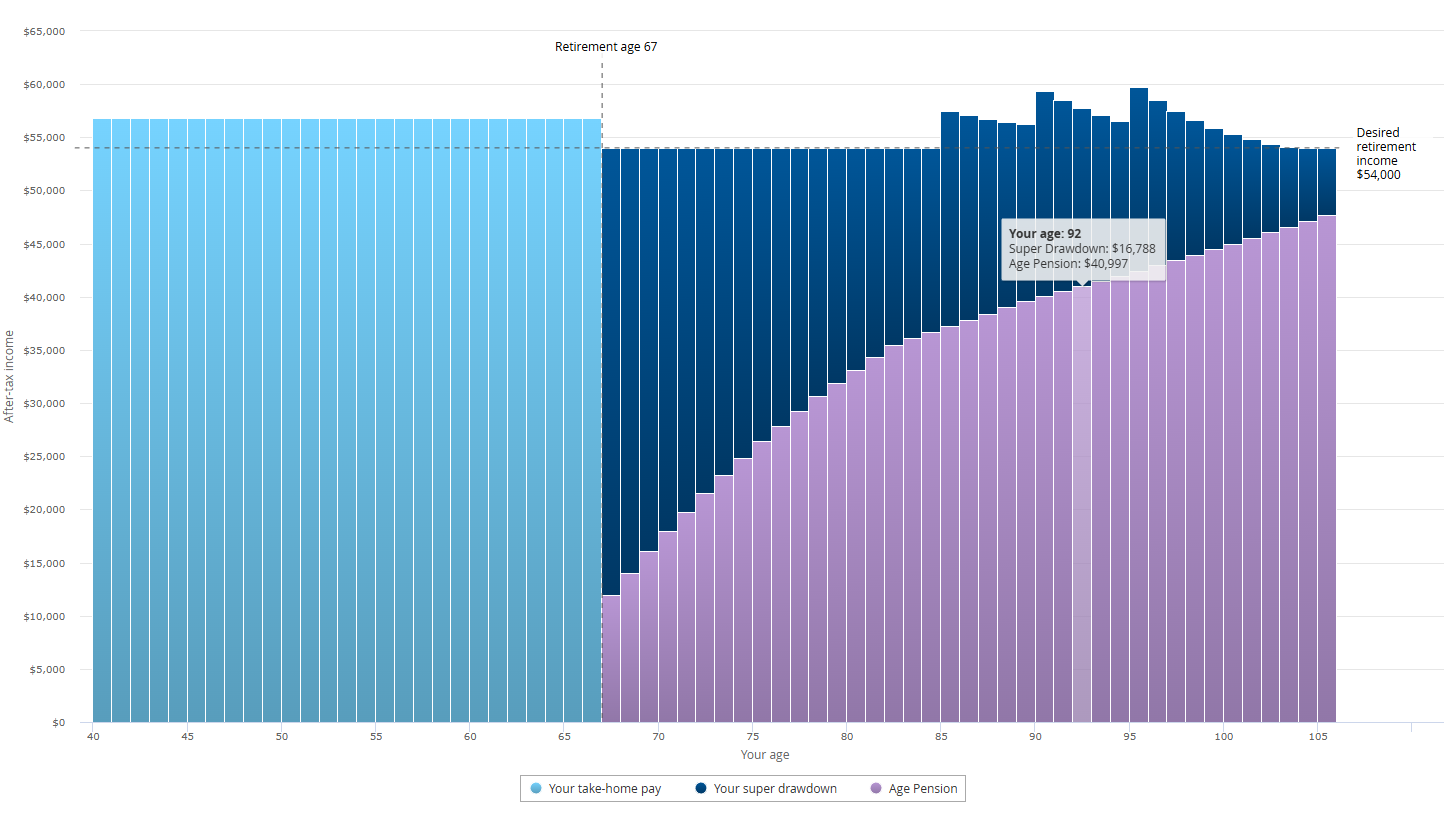

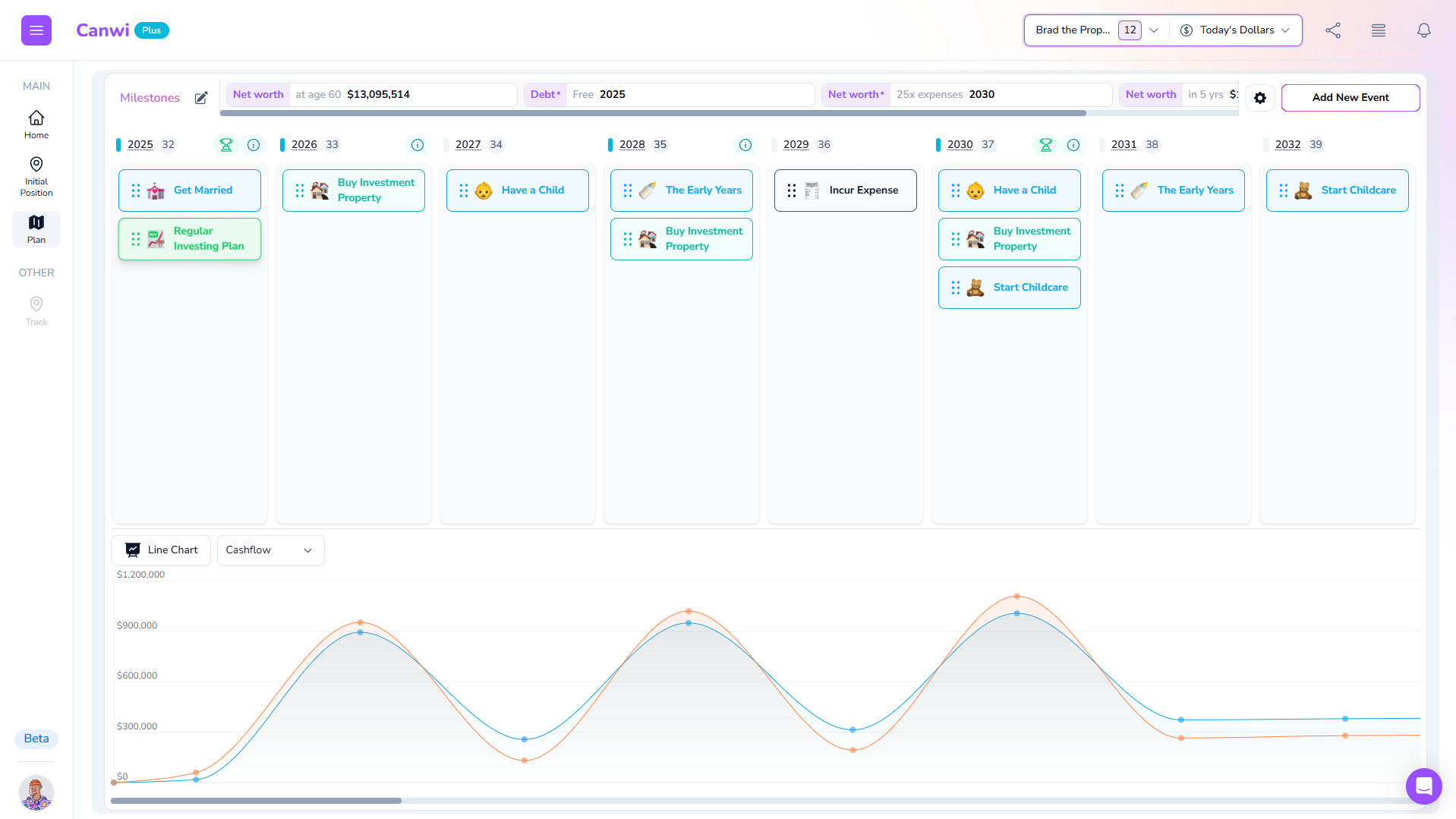

Canwi

Canwi was built specifically to address the gaps that show up across the tools above - particularly for Australians who want flexibility before 60, not just a projection of life after it.

Instead of starting with accounts, balances, or financial entities, Canwi starts with real-life decisions and shows how they ripple through your finances over time.

Buying a home. Taking parental leave. Making extra super contributions. Working part-time. Retiring early.

Those decisions are the plan - the maths is handled underneath.

✅ Pros

- Life-event-driven planning, not entity-driven modelling

- Built specifically for the Australian financial system (tax, super, government benefits)

- Automatically handles:

- purchase costs (e.g. stamp duty when buying property)

- contribution caps, limits, and carry-forward logic

- interactions between cashflow, tax, assets, and super

- Designed to model early retirement and pre-super “bridge years”

- Makes trade-offs explicit (e.g. retire earlier vs work longer vs spend less)

- Reduces the need to “know the tricks” upfront - the platform surfaces them as you plan

⚠️ Cons

- Less focused on adviser-grade reporting or professional plan documentation

- Not designed for users who want to manually control every formula or assumption

- Still evolving - depth is prioritised where it most impacts real decisions rather than every possible edge case

🎯 Best for

Australians who want to understand their options, explore trade-offs, and make confident decisions about early retirement - without needing to translate life events into financial entities or already know every rule.